Sunday, 25 February 2018 - 6:44pm

These past few weeks, I have been mostly drinking and working, in that order. Here's some stuff:

- I predicted the last financial crisis – now soaring global debt levels pose risk of another — Steve Keen in the Conversation:

Bernanke, who got the job as head of the US central bank because he was supposed to be the expert on what caused the Great Depression, didn’t even consider similar data that was available at the time, nor 1930s economist Irving Fisher’s thesis, which pointed the finger at the bursting of asset bubbles. Bernanke believed that credit “should have no significant macroeconomic effects”. […] Empirically, this is manifestly untrue, but economists turn a blind eye to this data because it doesn’t suit their preferred model of how banks operate. They model banks as if they are intermediaries that introduce savers to borrowers, not as originators of both money and debt. This deliberate blindness was, in a sense, excusable before the crisis. But it’s unforgivable after it – especially since central banks are actually coming out now and saying that this “Loanable Funds” model is a myth.

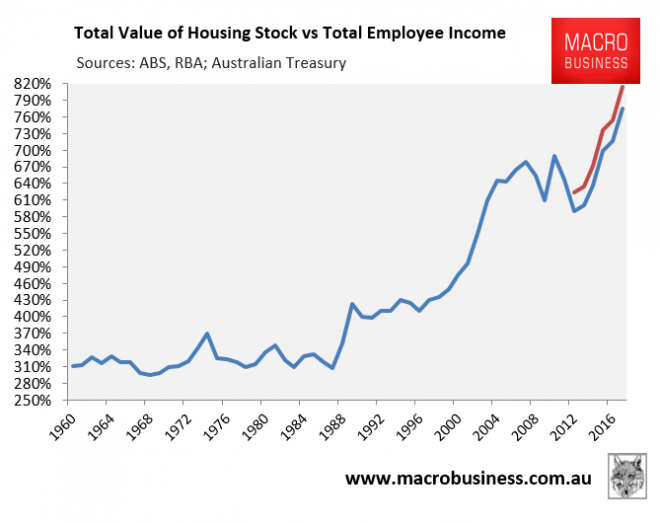

- Aussie housing valuations obliterate all records — Leith van Onselen at MacroBusiness:

The ABS on Tuesday released its property price data for the June quarter, which valued Australia’s dwelling stock owned by households at a record $6.39 trillion, whereas the total housing stock was valued at a record $6.73 trillion. As shown below, the total value of Australia’s dwelling stock owned by households was an all-time high 7.7 times employee incomes as at June 2017, up from 7.2 times incomes a year prior, whereas the total housing stock was valued at 8.2 times employee incomes:

- Bro Cat would like to hang out — The Oatmeal:

- There's a reason why anti-Muslim ideology hasn't found a home in Portugal — Robert Fisk, the Independent:

Thanks to the work of Italian scholar Fabrizio Boscaglia and Brazilian researcher Marcia Feitosa, we find [modern Portuguese poet Fernando] Pessoa espousing “our [Portuguese] great Arab tradition – of tolerance and free civilisation. It is in the manner in which we are the keepers of the Arab spirit in Europe that we will have a distinct individuality… Let us revenge the defeat inflicted by those from the North to our Arab ancestors. Let us redeem the crime we committed when we expelled from the peninsula the Arabs that civilised it.” Perhaps it’s no wonder that less than two years ago, Portugal’s Prime Minister Antonio Costa said that his country would receive 10,000 Syrian refugees – double the number it might have taken under the EU’s relocation programme. Compare that to the “protectors” of our Christian “civilisation” further east.

Sunday, 4 February 2018 - 5:19pm

This week… Oy! Reading schmeading:

- The death of Christianity in the U.S. — Miguel De La Torre in Baptist News Global:

The Evangelicals’ Jesus is satanic, and those who hustle this demon are “false apostles, deceitful workers, masquerading as apostles of Christ. And no wonder, for Satan himself masquerades as an angel of light. It is not surprising, then, if his servants also masquerade as servants of righteousness. Their end will be what their actions deserve” (2 Cor. 11:13-15, NIV). You might wonder if my condemnation is too harsh. It is not, for the Spirit of the Lord has convicted me to shout from the mountaintop how God’s precious children are being devoured by the hatred and bigotry of those who have positioned themselves as the voice of God in America.

- Austerity is an Algorithm — Gillian Terzis in Logic:

Things changed in December 2016, when the government announced that the system had undergone full automation. Humans would no longer investigate anomalies in earnings. Instead, debt notices would be automatically generated when inconsistencies were detected. The government’s rationale for automating the process was telling. “Our aim is to ensure that people get what they are entitled to—no more and no less,” read the press release. “And to crack down hard when people deliberately defraud the system.” The result was a disaster. I’ve had friends who’ve received an innocuous email urging them to check their MyGov account—an online portal available to Australian citizens with an internet connection to access a variety of government services—only to log in and find they’re hundreds or thousands of dollars in arrears, supposedly because they didn’t accurately report their income. Some received threats from private debt collectors, who told them their wages would be seized if they didn’t submit to a payment plan. Those who wanted to contest their debts had to lodge a formal complaint, and were subjected to hours of Mozart’s Divertimento in F Major before they could talk to a case worker. Others tried taking their concerns directly to the Centrelink agency on Twitter, where they were directed to calling Lifeline, a 24-hour hotline for crisis support and suicide prevention.

- A Eulogy for the Headphone Jack — Charlie Hoey in Medium:

Sound cards happen to carry sound most of the time, but they are perfectly happy measuring any AC voltage from -2 to +2 volts at 48,000 times per second with 16 bits of accuracy. […] To any headphone jack, all audio is raw in the sense that it exists as a series of voltages that ultimately began as measurements by some tool, like a microphone or an electric guitar pickup or an EKG. There is no encryption or rights management, no special encoding or secret keys. […] Smartphone manufacturers are broadly eliminating headphone jacks going forward, replacing them with wireless headphones or BlueTooth. We’re going to all lose touch with something, and to me it feels like something important.

- Australians pay more for education than the OECD average – but is it worth it? — Megan O'Connell in the Conversation, with obligatory Goodhart's Law warning. It would be interesting to see how the ratio of public to private spending correlates with the range of courses on offer:

Australians value education, so when looking at the OECD’s Education at a Glance 2017 report, it’s not surprising to see we spend more on education than average among comparable nations. However, it’s worth noting where the money comes from. A closer look at the data shows public funding for education in Australia is much less than the OECD average, with private funders (including families and students) footing the rest of the bill. When combining both public and private funding sources, our overall spending on education is 5.8% of GDP from primary to tertiary levels. As our Federal Education Minister has been quick to note, this is more than the OECD average of 5.2%. However, when looking at public expenditure, Australia, at 3.9% of GDP, is well below most OECD countries.

Tuesday, 30 January 2018 - 9:22pm

Well, I feel better now.

On 30/01/18 13:15, Talent Acquisition Team [company name witheld] wrote:

> Hello Matthew,

>

> We're writing to you regarding your application for the above position of

> [interchangeable anonymous cubicle drone] at [company name witheld].

>

> Unfortunately, we have not received your completed Talent Assessment so are

> unable to progress your application at this time. If you’re still interested in

> working with us, please refer to the [company name witheld] Careers

> <https://companynamewitheld.com>

> or LinkedIn page <https://www.linkedin.com/company/companynamewitheld> for opportunities.

>

> We wish you all the very best for your future career choices and hope to hear

> from you again soon.

>

> Warm regards,

>

> Talent Acquisition Team - [company name witheld]

Hi Warmly Regarding TAT,

That would be because your online application process set a cookie with a very limited expiry time given the amount of information I was expected to assemble, and deliberately cut me off (my working hypothesis at the time), or else just crashed or futzed up in some unidentifiable way.

I was a software developer in a past life, but - even so - was not inclined to report a bug, even if there were some self-evident way to do so. You see, the larger issue, to the determined jobseeker, arises from losing whole days to combing through job search websites which all screen-scrape each other, and consequently all index the same jobs, albeit with differently-dreadful database query interfaces. Once you have painstakingly whittled down a shortlist your patience and optimism levels are at a low ebb, while your bleak hopelessness and can't-give-a-fuckedness is soaring.

To my mind, ignorant as I am about the transition from HR to TATs (which appears to have happened about the time The Rock became Dwayne Johnson; coincidence?), the personal qualities required to submit, submit, and submit again in a lengthy and repeatedly failing multi-stage job application process (never mind what is required to get far enough to begin that process) are not necessarily consonant with what is desirable across all the roles in a large organisation. In the jargon of a hypothetical recruiter, I expect this to yield applicants who are less "warm and customer-focused" than they are "detail-oriented", as in "Dustin Hoffman turned in bravura performance as the detail-oriented Rain Man".

However, I am pleased to report that for you, the fine people of the Talent Acquisition Team, the news is all good. Given that the cascade of flaws, all the way up the recruitment chain from yorrasadunemployablelosr.com to your good selves, introduces so much baked-in randomness to the process, anything that you could personally add is negligible.

You are off the hook! After showing up for a morning coffee and apricot danish, you might as well spend the rest of the day in the pub! I only wish that I could join you there on the coalface of the optimally efficient job market. If you find your roster of talent too loaded with twenty-something boys who can't tear their gaze away from their shoes, just drag in a homeless person from the street. They're quirky! They're the new office character! They think outside the box, then go home to it!

Hope this has helped, and warm regards,

Matthew.

Sunday, 21 January 2018 - 8:05pm

This fortnight, I have been mostly working for money rather than knowledge:

- The historical context to Trump's 's***hole' remarks only makes them more outrageously shameful — Andrew Buncombe, the Independent:

Between 1956 and 1986, the country was dominated by the murderous dictators Francois “Papa Doc” Duvalier and his son, Baby Doc. Four years after Baby Doc fled to France, it seemed that Aristide, who swept to power with 70 per cent of the vote, was poised to bring change. So he might, had he not antagonised the country’s small elite or their supporters in Washington. If Donald Trump was interested in history he would know this. He would know the challenges Haiti has faced, and the way his own country has hampered its development. He would know how, even now, the US Embassy and State Department are major player in the country’s politics, throwing their support behind those candidates it approves of, and blocking the path of those it does not like.

- Why are doctors in the Middle East cosying up to foreign armies? — Robert Fisk, the Independent:

Jonathan Whittall of Medecins Sans Frontieres (MSF) first raised the alarm during and after the siege of Mosul when doctors and medical personnel sometimes allowed local security forces to check the identity of patients entering their hospitals or aid centres. “Sometimes they gave the names of patients to the local secret services,” Whittall told The Independent. “Horrific compromises were made to work hand-in-hand with the international military coalition. The wounded were often not treated as patients but as suspects. This fundamentally compromises the trust patients have in medics. And this makes our work less effective”.

Sunday, 7 January 2018 - 11:03pm

This week, I have been mostly reading:

- The costs of a casual job are now outweighing any pay benefits — Joshua Healy and Daniel Nicholson:

One in four Australian employees today is a casual worker. Among younger workers (15-24 year olds) the numbers are higher still: more than half of them are casuals. These jobs come without some of the benefits of permanent employment, such as paid annual holiday leave and sick leave. In exchange for giving up these entitlements, casual workers are supposed to receive a higher hourly rate of pay – known as a casual “loading”. But the costs of casual work are now outweighing the benefits in wages.

- 'The S-word': how young Americans fell in love with socialism — Chris McGreal in the Guardian:

Americans who came of age during the cold war saw socialism being characterized as the close cousin of Soviet communism, and state-run healthcare as a first step to the gulags. There are still those attempting to keep the old scare stories alive. It was the old cold war warriors who helped detoxify socialism for younger Americans when the Tea Party and Fox News painted Obama – a president who recapitalised the banks without saving the homes of families in foreclosure – as a socialist for his relatively modest changes to the healthcare system. Then came Sanders.

- How Orwell used wartime rationing to argue for global justice — Bruce Robbins in Aeon:

There could be no anti-fascist solidarity unless the exploited Indians could believe that a more just distribution of the world’s resources was possible – that global inequality could be changed. The popularity of rationing proved that, with the right incentive, the citizens of the more prosperous countries were willing to live on less. If this had happened in wartime, it might also happen in peacetime. There were other ways to divide the pie. No law of nature or economics pegged British consumption and Indian consumption at a 12-to-one ratio forever.

Sunday, 31 December 2017 - 6:29pm

This week, I have been mostly reading:

- How I Got Fired From a D.C. Think Tank for Fighting Against the Power of Google — Zephyr Teachout in the Intercept:

In June, when the European Union fined Google $2.7 billion for abusing its dominant position to serve itself and quash competition, the Open Markets team put out a press statement that was entirely consistent with its longstanding position. It praised the EU’s action, and argued that American antitrust authorities should also look at Google’s use of its search power to leverage its influence in other markets. New America’s leadership must have gotten an earful. Within 72 hours, New America’s president, Anne-Marie Slaughter, told Lynn that he — and all of us on the Open Markets team — had to leave. As the New York Times reported yesterday, Slaughter emailed Lynn to say that “the time has come for Open Markets and New America to part ways,” and the email accused Lynn of “imperiling the institution as a whole.” (After the Times story was published, Slaughter tweeted that the article was “false,” though she later added, “facts are largely right, but quotes are taken way out of context and interpretation is wrong.”)

[Some additional context provided by the Intercept] - Racism is real, race is not: a philosopher’s perspective — Adam Hochman in the Conversation:

From a scientific perspective, the best candidate for a synonym for “race” is “subspecies” (the classification level below “species” in biology). When scientists apply the standard criteria to determine whether there are subspecies/races in humans, none are found. In chimpanzees yes, but in humans no. Racial classification is unscientific. However, humanities scholars have their own justifications for race-talk. Many argue that while there are no biological races, there are social races. Race, as philosophers put it, is a social kind. In my view, the redefinition of race as a social kind has been a major mistake. Most people still think of race as a biological category. By redefining it socially, we risk miscommunicating with each other on this fraught topic.

- Stylised Facts — Robert Skidelsky Wow. This is great. Lots in here, but this jumped out at me, given my current interests:

Though Kaldor was concerned with long-run growth and Keynes with the short- run management of demand, there was no contradiction between the two, since post-war Keynesians like Kaldor assumed that Say’s Law was now guaranteed by Keynesian full employment policy. This re-established the long-run growth agenda of the classical economists. So the Keynesian economists of that day produced growth models – Harrod-Domar, Solow, Rostow, etc. – geared chiefly to the problems of the developing world. This growth orientation did mean though that Kaldor was as much concerned with the conditions of supply as demand, something evident in his 1966 inaugural lecture. Kaldor was heir to the German economist Friedrich List, in that he regarded premature free trade as an obstacle to growth for those countries in the business of catching up with the leaders. Countries should seek to develop their dynamic rather than simply exploit their static comparative advantages. This required policies of protection and import substitution. Kaldor was passionately opposed to static equilibrium analysis.

- After such unexpected success in 2017, what does Jeremy Corbyn have planned for 2018? — Richard Seymour in the Independent:

The result didn’t come from nowhere. It was a vindication of the strategy outlined by Corbyn when he won the leadership in 2015. To rebuild its electoral base, Labour had to rebuild itself as a membership party. It had to recruit previous non-voters, above all the young and the poor, shamelessly written off by pollsters and most politicians. It had to move sharply to the left, and stop trying to appease the media and the Conservatives. Corbyn’s point has been proven, far more quickly than even his supporters expected. More importantly, the form of organised distrust of the members evinced by the old managerial guard, has been discredited. Labour’s members have shown more insight into contemporary Britain than the majority of MPs. And finally, after many years in which activists themselves distrusted the party form, it proved its worth: for all its limits, this scale of organisation can change the country.

- Australian national accounts – government spending drives growth — Bill Mitchell:

The ABS released the – June-quarter 2017 National Accounts data – today (September 6, 2017), which showed that real GDP had risen by 0.8 per cent in the June-quarter 2017. Annual growth (last four quarters) was just 1.8 per cent around half the trend rate before the GFC. The striking result was that public spending (consumption and investment) contributed 0.8 percentage points to the growth rate – which means that without that contribution, real GDP growth would have been zero in the June-quarter 2017. Private consumption expenditure contributed 0.4 points, although the household saving ratio fell again indicating the tenuous nature of relying on this growth with flat wages. Private investment spending was negative. Net exports were stronger with export volumes strong in the face of the falling terms of trade. Overall, the growth is unbalanced – relying on lumpy public investment spending and credit-driven private consumption growth. The outlook is thus uncertain.

Sunday, 24 December 2017 - 5:52pm

This week, I have been mostly reading:

- The U.S. Spy Hub in the Heart of Australia — Ryan Gallagher for the Intercept and the Australian Broadcasting Corporation:

Emily Howie, director of advocacy and research at Australia’s Human Rights Law Centre, said the Australian government needs to provide “accountability and transparency” on its role in U.S. drone operations. “The legal problem that’s created by drone strikes is that there may very well be violations of the laws of armed conflict … and that Australia may be involved in those potential war crimes through the facility at Pine Gap,” Howie said. “The first thing that we need from the Australian government is for it to come clean about exactly what Australians are doing inside the Pine Gap facility in terms of coordinating with the United States on the targeting using drones.”

- Marketising Social Care: Why we need to talk about the NDIS — Fiona Macdonald in Arena:

As the Productivity Commission continues to look for new ways to introduce ‘greater user choice, competition and contestability’ in human services, the marketisation of social care in Australia proceeds apace. Here, as in the other liberal states (the United States, Canada and Britain) and in many European countries, care provisions for children, the elderly, the ill and people with disabilities are increasingly likely to be commodities purchased by consumers through markets. We are in the middle of the rollout of the National Disability Insurance Scheme (NDIS) and just this year Consumer-Directed Care (CDC) has been introduced in home care for the aged. Yet there has been relatively little public discussion about the likely downsides of these latest moves to marketise social care in Australia. The provision of care through ‘cash-for-care’ or voucher schemes—involving the allocation of public funding to individual care users to purchase their care services on the market—is increasingly widespread. While lauded by proponents as empowering—by placing control in the hands of care users—and seen as increasing efficiency, the construction of care markets in which individuals are care ‘consumers’ does not necessarily produce good outcomes for people requiring care. At the same time, marketised care economies are mostly built on large workforces of low-paid workers in insecure work with poor working conditions. The mixed origins of cash-for-care schemes provide an indication of why, despite these problems, they have some appeal for consumer and care-user advocates

- Social Security: Still The Most Efficient Way To Provide Retirement Income — Dean Baker in the Huffington Post:

A big part of the benefit of Social Security is that it is very efficient. The administrative costs of the retirement portion of the program are just 0.4 percent of what is paid out in benefits each year. By comparison, the costs of even relatively well-run privatized systems, like those in Chile or the United Kingdom, are 10-15 percent of benefits. That difference would amount to $80 billion a year (close to $1 trillion over a ten-year budget horizon) being paid out to the financial industry instead of to retirees.

- Trump Sends More Troops Into The Afghanistan Meatgrinder — Ted Rall:

- The Taliban Tried to Surrender and the U.S. Rebuffed Them. Now Here We Are. — Ryan Grim at the Intercept:

For centuries in Afghanistan, when a rival force had come to power, the defeated one would put down their weapons and be integrated into the new power structure — obviously with much less power, or none at all. That’s how you do with neighbors you have to continue to live with. This isn’t a football game, where the teams go to different cities when it’s over. That may be hard for us to remember, because the U.S. hasn’t fought a protracted war on its own soil since the Civil War. So when the Taliban came to surrender, the U.S. turned them down repeatedly, in a series of arrogant blunders spelled out in Anand Gopal’s investigative treatment of the Afghanistan war, “No Good Men Among the Living.” Only full annihilation was enough for the Bush administration. They wanted more terrorists in body bags. The problem was that the Taliban had stopped fighting, having either fled to Pakistan or melted back into civilian life. Al Qaeda, for its part, was down to a handful of members. So how do you kill terrorists if there aren’t any?

- Dozens of Companies Are Using Facebook to Exclude Older Workers From Job Ads — Julia Angwin, Noam Scheiber, and Ariana Tobin for ProPublica and the New York Times:

Verizon is among dozens of the nation's leading employers — including Amazon, Goldman Sachs, Target and Facebook itself — that placed recruitment ads limited to particular age groups, an investigation by ProPublica and The New York Times has found. The ability of advertisers to deliver their message to the precise audience most likely to respond is the cornerstone of Facebook’s business model. But using the system to expose job opportunities only to certain age groups has raised concerns about fairness to older workers. Several experts questioned whether the practice is in keeping with the federal Age Discrimination in Employment Act of 1967, which prohibits bias against people 40 or older in hiring or employment. Many jurisdictions make it a crime to “aid” or “abet” age discrimination, a provision that could apply to companies like Facebook that distribute job ads.

- 55 Ways Donald Trump Structurally Changed America in 2017 — Nick Tabor, New York Magazine:

[…] given that the congressional year has otherwise been marked by turmoil and inaction, and given the high staff turnover and the parade of scandals at the White House, it’s been easy to miss what this administration has already done. In the background, Donald Trump’s Cabinet members and their collaborators have been working hard to deliver on Steve Bannon’s vision of dismantling the “regulatory state.” With Trump’s blessing, they have made drastic, structural changes on education, immigration, environmental protections, broadcasting and internet laws, and rules of military engagement, among other issues. Most often the changes have taken direct aim at Obama’s legacy, but some apply to regulations and programs that date back decades.

- Who is Reality Winner? — Kerry Howley in New York Magazine:

Ronald was intellectually engaged, though never, during his marriage, employed, and Reality’s parents separated in 1999, when she was 8. Two years later, when the Towers fell, Ronald held long, intense conversations about geopolitics with his daughters. He was careful to distinguish for them the religion of Islam from the ideologies that fueled terrorism. “I learned,” says Reality, “that the fastest route to conflict resolution is understanding.” She credits her father with her interest in Arabic, which she began studying seriously, outside school and of her own accord, at 17. It was this interest in languages that eventually drew her into a security state, unimaginable before 9/11, that she chose to betray. Fifteen years after those first conversations with her father, Reality’s interest in Arabic would be turned against her in a Georgia courtroom, taken as evidence that she sympathized with the nation’s most feared enemies.

Sunday, 10 December 2017 - 4:00pm

This week, I have been mostly setting up a super-secret project, rather than reading:

Sunday, 3 December 2017 - 5:04pm

This week, I have been mostly reading:

- The loanable funds hoax — Lars P. Syll:

The age-old belief that Central Banks control the money supply has more an more come to be questioned and replaced by an ‘endogenous’ money view, and I think the same will happen to the view that Central Banks determine “the” rate of interest.

- Have We Learned Our Lessons from the Financial Crisis? Rewriting History Is Not a Good Sign — Dean Baker:

As I have argued elsewhere, it is convenient for economists to blame the financial crisis rather than the bubble, because finance can be complicated. After all, who knew that AIG had written $600 billion worth of credit default swaps on mortgage backed securities? On the other hand, the bubble was pretty simple. We had an unprecedented nationwide run-up in house prices with no plausible explanation in the fundamentals of the housing market. Rents were going nowhere and vacancy rates were already at record highs before the crash. And the bubble was clearly driving the economy. Residential construction was at a record high as a share of GDP and consumption boomed based on the bubble generated housing wealth. When the bubble burst, there was no source of demand that could replace the lost construction and consumption, which is the story of the Great Recession.

- Sometimes giving a person a choice is an act of terrible cruelty — Lisa Tessman in Aeon:

Sometimes, it’s pure bad luck that puts someone in the position of having to choose between wrongdoings. However, much of the time, choice doesn’t take place in contexts that are shaped entirely accidentally. It takes place in social contexts. Social structures, policies, or institutions can produce outcomes that favour some groups of people over others in part by shaping what kinds of choices people get to – or have to – face. Members of some social groups might face mostly bad choices, in the sense that their choices are between alternatives, all of which are disadvantageous to them. But there’s another sense in which the choices might be bad: these might be choices between alternatives, all of which make them fail in their responsibilities to others. The American Health Care Act, which was considered in the United States House and Senate, would have created moral dilemmas by offering people without high incomes – especially if they were also women, or old or sick – a range of bad options. It would have forced some parents to make choices between two equally unthinkable options, such as the ‘choice’ to sacrifice one child’s health care for another’s.

Which Keynesianism?

I posted this enormous torrent of blather on Blackboard the other day. It's mostly a restatement of stuff I've said before, but I'll repost it here for the purposes of copying and pasting in the likely case I have to restate it yet again elsewhere.

Because I've been studying economics for the last few years, rather than sticking to the curriculum and dutifully cultivating my employability, I feel obliged to chip in with a cautionary note: Almost all of the academic economists, and their policy prescriptions, which are characterised as Keynesian have nothing to do with the work of Keynes.

The post-war economic order established at Bretton Woods is conventionally understood as being Keynesian, but in fact Keynes was railroaded by the US representative Harry Dexter White, who insisted upon the system of fixed exchange rates pegged to the US dollar, with global dependency on holding US dollar reserves being greatly to America's benefit; the US gained the benefit of cheap foreign imports sold to acquire those reserves. Neither was Keynes responsible for the "Bretton Woods institutions", the World Bank and the IMF. His plan for regulating and settling international financial flows was considerably more humane than the usurious loans and standover tactics these institutions became notorious for.

Even "progressive" and "liberal" economists like Paul Krugman and Joe Stiglitz are members of the school of "New Keynesianism", a product of what Paul Samuelson called the "Neoclassical Synthesis"; taking some of the superficial trappings of Keynes' work and melding it with the earlier "neoclassical" school of economics, which Keynes actually intended to entirely overturn. Neoclassical models of the economy ignore the role of money and banking, believing that all economic transactions are ultimately barter transactions, and that money is therefore said to be "neutral", and banking is just redistribution of loanable funds, ultimately of no macroeconomic effect. Keynes wrote of this "Real-Exchange economics" (in an article unfortunately unavailable via SCU):

Now the conditions required for the "neutrality" of money, in the sense in which it is assumed in […] Marshall's Principles of Economics, are, I suspect, precisely the same as those which will insure that crises do not occur. If this is true, the Real-Exchange Economics, on which most of us have been brought up and with the conclusions of which our minds are deeply impregnated, […] is a singularly blunt weapon for dealing with the problem of Booms and Depressions. For it has assumed away the very matter under investigation.

This is the answer to Queen Elizabeth's question on how economists failed to see the Global Financial Crisis (GFC) coming; if the financial sector is macroeconomically neutral, as the neoclassicals claim, there cannot be any financial crises. However, outside the neoclassical tradition, the normal functioning of the economy, and the pathologies leading to crises, are well understood:

- The Chartalists determined that all money is credit, ultimately issued by the state. Michael Hudson recently did some exhaustive historical work on this, which David Graeber popularised in his book Debt: the First 500 Years.

- Wynne Godley showed how currency-issuing states must spend more than they tax if the private sector is to have the money necessary to spend and save.

- Irving Fisher identified the role of debt deflation in turning a rush to liquidate debt into an ongoing crisis where outstanding debts become impossible to repay.

- Hyman Minsky's financial instability hypothesis extended Fisher's work to describe how financial crises arise from the normal workings of a capitalist economy.

- Keynes implicitly regarded the money economy as a tool for allocating real resources in pursuit of public policy objectives, a principle explicitly formulated by Abba Lerner as "functional finance". This is in opposition to the neoclassical intuition that a household is like an individual, a firm is like a household, and a government is like a firm; therefore a government must follow the principles of "sound finance" and "live within its means".

- All of the above are incorporated in the teachings of "Post-Keynesian" economics, which Keynes' biographer Robert Skidelsky considers closest to Keynes' own thinking. The sub-field of Modern Monetary Theory (MMT) synthesises all of these into a single coherent framework for analysing the economies of countries which issue their own currency.

By the end of World War II, functional finance was so well established as to be almost universally understood to be common sense. The 1945 White Paper on Full Employment in Australia, prepared for John Curtin by H. C. "Nugget" Coombs, and based on the principles in Keynes' General Theory of Employment, Interest, and Money, declared:

It is true that war-time full employment has been accompanied by efforts and sacrifices and a curtailment of individual liberties which only the supreme emergency of war could justify; but it has shown up the wastes of unemployment in pre-war years, and it has taught us valuable lessons which we can apply to the problems of peace-time, when full employment must be achieved in ways consistent with a free society.

In peace-time the responsibility of Commonwealth and State Governments is to provide the general framework of a full employment economy, within which the operations of individuals and businesses can be carried on.

Improved nutrition, rural amenities and social services, more houses, factories and other capital equipment and higher standards of living generally are objectives on which we can all agree. Governments can promote the achievement of these objectives to the limit set by available resources.

(Emphasis mine.) As expressed by MMT, currency-issuing governments are not fiscally constrained. The only limits on public policy are real resource limits. During the last UK election campaign, Theresa May was vehemently insisting "there is no magic money tree". But in fact there is: it's called the Bank of England (we have the Reserve Bank of Australia), and Her Majesty's Treasury has an unlimited line of credit there. Whenever the government wants to spend, the Bank of England just credits the accounts of commercial banks. I was delighted when while campaigning May was confronted by a furious protester wanting to know "Where's the magic doctor tree? Where's the magic teacher tree?" The policy limits we should be worried about are real resources (including people), not money.

Nevertheless, mainstream economists and politicians believe, in some vague way, that (as Stephanie Kelton puts it) "money grows on rich people". So it's not surprising to read already on the discussion boards here that Keynesianism is all very desirable, but how will the federal government pay for it? This is a meaningless question. The government will pay for it like it pays for anything: by spending the money into existence. That's where all money comes from, net of private sector credit creation. Logically, it can't come from anywhere else. If the government were to try to achieve fiscal (or, conflating governments and firms again, "budget") surpluses over the long term by taxing more than they spend, as neoclassicals, including New Keynesians, recommend, they would merely be draining savings from the private sector for no good reason. State-issued money is an IOU, a tax credit. When the credit is redeemed it ceases to exist. The government doesn't have to tax in order to spend. It has to spend in order to tax. Think about it: where else would the first dollar ever taxed come from?

Now you might be thinking, hang on: what about the most fiscally responsible government we've ever had (Howard/Costello) and their record run of "budget" surpluses? The economy was going gangbusters! Okay, here's the fiscal balance for that period:

As with every currency-issuing sovereign state in history, deficits are the rule, not the exception. Here's what happened to private sector debt over the same period:

(Data from the Bank of International Settlements and OECD.) As soon as the government started taxing more than it spent, private sector debt took off, and subsequent fiscal deficits were insufficient to reverse the damage. Notably, at the same time household debt overtook corporate debt, as credit was used to sustain consumer demand, not to mention standards of living, rather than for investment in productive capacity. Australia "Nimbled it, and moved on", and to hell with the consequences.

Australia recently passed two milestones of note: total private sector debt (the blue line above) exceeded 200% of GDP — at roughly the level that Japan's private debt was at in the early 90s when its real estate bubble burst — and bank equity in residential real estate passed 50%. That's 50% of the total residential real estate stock, not just houses built in the last x years. Minsky describes the path to financial collapse as progressing through the stages of "hedge finance", then "speculative finance", and finally "Ponzi finance". When you see phenomena like interest-only mortgages — where the principal is never repaid, on the assumption that housing prices only ever go up, and the debt will be settled whenever you sell the property, presumably pocketing a tidy and lightly-taxed capital gain at the same time — you know which stage you're in.

So why does nobody in mainstream politics or economics know anything about this? To put it succinctly, because neoliberalism. On the left, the "balancing the books" rhetoric serves a useful purpose: it gives you a disingenuous pretext to do what you want to do anyway that is compatible with the dominant paradigm. As Randy Wray said at a recent MMT conference:

"[Progressives] link the good policies they want to 'we'll tax the rich to pay for it'. So when you point out we don't need to tax the rich to pay for it, they're just crestfallen because they want to tax the rich. So I say 'Of course we should tax the rich. Why? They're too rich.' You don't need any other argument than that."

Taxes drive demand for the currency. If you know you have to pay taxes, you will work to get the money to pay for it. It's a coercive way for the government to mobilise labour to achieve its policy objectives, but assuming policy is arrived at democratically, it's relatively fair and vastly preferable to the autocratic alternative of having a gun put to your head. Taxes are also a fiscal instrument that can be used to discourage certain kinds of behaviour, and harmful social phenomena (like income inequality).

In the neoliberal era, that's why Australia has a retrospective tax on education called HECS-HELP, which in turn is why SCU has no school of history, or philosophy, or in fact any of the traditional academic disciplines. Students know that their education will be retrospectively taxed, so they can't afford to choose disciplines unlikely to offset that tax with increased earnings. There are twice as many universities as there were in 1988, but the new ones are glorified vocational colleges with next to no permanent academic staff. Australian post-Keynesian economist Steve Keen, who correctly predicted — and more importantly, explained — the GFC, subsequently lost his job at the University of Western Sydney when they closed down their economics department. Who needs academic economics when you have business studies courses, after all? He ended up at Kingston University in London, another young neoliberal institution, where last year he was given an ultimatum to spend more hours teaching or take a significant pay cut. He's ended up having to put his hat out for donations from the public in order to continue his work as a public intellectual.

Why would public policy function like this? Why would policy makers want a population uneducated about how the world actually works, and instead merely trained in how to work in it? Why is the conventional wisdom so full of assertions that are demonstrably untrue, and profoundly damaging to society? Paul Samuelson, author of the macroeconomics textbook that gave generations of undergraduates a completely misleading interpretation of Keynes' work explained this in an interview:

I think there is an element of truth in the view that the superstition that the budget must be balanced at all times [is necessary]. Once it is debunked [that] takes away one of the bulwarks that every society must have against expenditure out of control. There must be discipline in the allocation of resources or you will have anarchistic chaos and inefficiency. And one of the functions of old fashioned religion was to scare people by sometimes what might be regarded as myths into behaving in a way that the long-run civilized life requires. We have taken away a belief in the intrinsic necessity of balancing the budget if not in every year, [then] in every short period of time. If Prime Minister Gladstone came back to life he would say "uh, oh what you have done" and James Buchanan argues in those terms. I have to say that I see merit in that view.

So basically, belief in myths must be maintained among the general population wherever doing so provides support for the elite political preference for small government, i.e. for control over the economy to be exercised by private finance rather than public fiscal policy. This is what neoliberalism fundamentally is, an Orwellian fiction imposed on a deliberately dumbed-down populous, with access to the truth as much the reserve of a select educated elite as ever. "Long-run civilised life" has been restored, thanks to neoliberalism's making of the 21st century by its un-making of the 20th.

I could go on forever (evidently) but others explain all this better than I:

- Here's a short interview with Steve Keen explaining how neoliberal austerity economics leads inevitably to financial crises.

- Stephanie Kelton is probably the best person to explain MMT to a general audience. Watch her describe the Angry Birds Approach to Understanding Deficits in the Modern Economy.

- Here's Bill Mitchell explaining in 15 minutes how fiscal policy works in the real world.

- Warren Mosler explains here why fiscal deficits are generally desirable. If you find reading easier than listening, I recommend Warren's slim volume (and even slimmer PDF file) Seven Deadly Innocent Frauds of Economic Policy.

If you have read this far, I admire your tenacity.