reading

Sunday, 18 September 2016 - 6:08pm

This week, I have been mostly reading:

- The German current account surplus requires deficits elsewhere — Edward Harrison at Credit Writedowns Pro:

With the periphery’s downturn came austerity and internal devaluation. And this has meant two adjustments. First, the EU as a whole has moved from a roughly balanced external position to a net creditor position as the German and Dutch export-led model is forced onto the periphery via internal devaluation used to achieve export competitiveness. Second, the Germans and Dutch have been forced to turn elsewhere to maintain their mercantilist trading stance. And they have found willing buyers in Asia and the emerging markets writ large. […] there is no mechanism in the current global currency system to correct these imbalances except through balance of payments crisis and the rise of protectionist populist politicians.

- Monopoly’s New Era — Joe Stiglitz in Project Syndicate:

Today’s markets are characterized by the persistence of high monopoly profits. The implications of this are profound. Many of the assumptions about market economies are based on acceptance of the competitive model, with marginal returns commensurate with social contributions. This view has led to hesitancy about official intervention: If markets are fundamentally efficient and fair, there is little that even the best of governments could do to improve matters. But if markets are based on exploitation, the rationale for laissez-faire disappears. Indeed, in that case, the battle against entrenched power is not only a battle for democracy; it is also a battle for efficiency and shared prosperity.

- ‘Smart’ Dildo Company Sued For Tracking Users’ Habits — Sara Morrison at Vocative chronicles a new low in the Internet of Things:

A few weeks ago, two researchers told the Defcon hacking convention audience that We-Vibe “smart” sex toys send a lot of data about their users back to the company that makes them. According to Courthouse News, one We-Viber took this news hard. A woman known only as “N.P.” filed a class action civil suit in a federal court in Illinois against Standard Innovation, which makes the We Vibe line of sex toys and corresponding app.

- The Free Market Isn’t Really Free — Robert Reich in Literary Hub:

In the United States, those with power and resources rarely directly bribe public officials in order to receive specific and visible favors, such as advantageous government contracts. Instead, they make campaign contributions and occasionally hold out the promise of lucrative jobs at the end of government careers. And the most valuable things they get in exchange are market rules that seem to apply to everyone and appear to be neutral, but that systematically and disproportionately benefit them. To state the matter another way, it is not the unique and perceptible government “intrusions” into the market that have the greatest effect on who wins and who loses; it is the way government organizes the market.

- Trending News — Nick Anderson, Truthdig:

- Isn’t it Time to Stop Calling it “The National Debt”? How about Government-Issued Assets instead? — Steve Roth at Evonomics:

The government has committed itself to issuing bonds for archaic reasons, so it needs to roll over its “debt.” Old bonds mature, the government pays them off and issues new ones to replace them. Unendingly, for decades and centuries. But the stock of government-issued assets just keeps growing — as it should and must in a growing economy. Those government-issued assets are a necessary lubricant for the operation of the private-sector economy. As the economy gets bigger, more of those assets are needed, as a kind of giant “pool” or buffer stock to avoid transactional lockups.

- Robert Samuelson Is Right on GDP — Dean Baker:

The measure of GDP is useful in assessing the health of an economy and society in the same way that weight is a useful measure in assessing a person's health. If a person is five feet and ten inches and weighs 300 pounds, then it is likely they have a problem. On the other hand, they can weigh 160 pounds and still have an inoperable tumor. We would want to know the person's weight to assess their condition, but it will not tell us everything we need to know to evaluate their health. In the same vein, we identify countries with high per capita GDP, but enormous inequality. It is hard to view these as success stories, since most of the population would not be benefiting from the strength of the economy.

- What Can Donald Trump Teach Us About the National Debt? — Dean Baker again:

Another much larger form of commitment is the rents that private individuals and corporations will earn from the patent and copyright monopolies that the government granted them. These rents are the difference between the monopoly price and free market price. In the case of prescription drugs alone, the rents are now in the neighborhood of $380 billion annually, or more than 2.0 percent of GDP. This is effectively the money the government paid the drug companies to do research. Add in the higher price for patents in other areas and copyrights on everything from software to computer games, and we may be talking about more than $1 trillion a year ( at 5.5 percent of GDP). That is a huge burden that we are passing on to our children.

- All of the problems Universal Basic Income can solve that have nothing to do with unemployment — Olivia Goldhill at Quartz:

There’s also some hope that UBI would allow both our employment and leisure time to become more fulfilling. Currently, millions of people are employed in what anthropologist David Graeber calls “bullshit jobs”—work that serves no real purpose, and is simply a way to fill time and provide salaries. One YouGov survey found that 37% of Brits think their jobs are meaningless. But under UBI, Bregman believes we would have the financial freedom to pursue useful and worthwhile work.

- Surviving Climate Change — Ian Welsh:

Make sure you have friends, locally, and that your neighbours know and like you. People who are well-liked by a lot of people are far more likely to survive bad times than those who aren’t. And having really good friends wherever you may have to flee to, if it comes to that, is wise.

Make sure you have friends, locally, and that your neighbours know and like you. People who are well-liked by a lot of people are far more likely to survive bad times than those who aren’t. And having really good friends wherever you may have to flee to, if it comes to that, is wise. - After Distancing Herself From Bill Clinton’s Economic Policies, Hillary Wants Him as Mr. Economic Fix It — Yves Smith, Naked Capitalism:

Needless to say, if Hillary doubts she can get the job done with her Cabinet and if needed, a czar here or there, and needs to bring in Bill too, this is an admission that her vaunted experience is not what it is cracked up to be. Hillary has the classic resume of someone who has failed upward: a series of every-splashier job titles, but with no or negative accomplishments.

- Trumping the critics — David F. Ruccio:

The only real issues from the government creation of money are (1) timing and (2) who benefits. Obviously, creating more money under conditions at or close to full employment has implications that are very different from a situation characterized by less than full employment (as has been the case for the past eight years). If resources are not being fully utilized, more money (helicopter or otherwise) does not lead to hyper-inflation. So, the critics who claim that, under current conditions (with millions of people who are unemployed or underemployed), creating more money is inflationary are simply wrong. As for who benefits, that’s the real controversy—and the issue that is rarely discussed. Creating money to finance purchases of private debt from banks obviously improves bank balance sheets (and the incomes of their owners and the power wielded by the boards of directors) but it doesn’t necessarily stimulate economic growth (if banks are unwilling to lend, because for them it’s not profitable), and it doesn’t help homeowners and others who are drowning in debt.

Sunday, 11 September 2016 - 7:49pm

This week, I have been mostly reading:

- Imagining a New Bretton Woods — Yanis Varoufakis in Project Syndicate:

Above all, the new system would reflect Keynes’s view that global stability is undermined by capitalism’s innate tendency to drive a wedge between surplus and deficit economies. The surpluses and deficits grow larger during the upturn, and the burden of adjustment falls disproportionately on debtors during the downturn, leading to a debt-deflationary process that takes root in the deficit regions before dampening demand everywhere. To counter this tendency, Keynes advocated replacing any system in which “the process of adjustment is compulsory for the debtor and voluntary for the creditor” with one in which the force of adjustment falls symmetrically upon debtors and creditors.

- Yes, the Economy Is Rigged, Contrary to What Some Economists Try to Tell You — Dean Baker summarises the things that have been occupying his mind lately, including:

In Europe and Japan, CEOs are also well-paid, but they tend to get a third or a quarter of what our CEOs earn. This matters not only because of the pay the CEOs get, but also because of its impact on pay structures throughout the economy. It is now common to see top executives of non-profit hospitals, universities, or private charities get salaries of more than $1 million a year. They argue that they would get much more working for a corporation of the same size. And, this money comes out of the pockets of the rest of us.

- Inflation Targeting and Neoliberalism — Gerald Epstein interviewed at TripleCrisis:

I see this as part of a whole neoliberal approach to central banking. That is, the idea that the economy is inherently stable, it will inherently reach full employment and stable economic growth on its own, and so the only thing that the macro policymakers have to worry about is keeping a low inflation rate and everything else will take care of itself. Of course, as we’ve seen, this whole neoliberal approach to macroeconomic policy is badly mistaken. […] This approach, I think, really has contributed to enormous financial instability. Notice that this inflation targeting targets commodity inflation. But what about asset bubbles, that is, asset inflation? There’s no attempt to reduce asset bubbles like we had in subprime or in real estate bubbles in various countries. That is another kind of inflation that could have been targeted.

- Robert Mundell, evil genius of the euro — Greg Palast in the Guardian:

Mundell explained to me that, in fact, the euro is of a piece with Reaganomics: "Monetary discipline forces fiscal discipline on the politicians as well." And when crises arise, economically disarmed nations have little to do but wipe away government regulations wholesale, privatize state industries en masse, slash taxes and send the European welfare state down the drain.

- Facebook Reactions and the Happiness Paradigm — Jenny Davis at the Society Pages:

These emoji express sadness and anger as a little bit silly, not too threatening, not too real. “Like” might not be the appropriate response to the passing of a loved one, but bulbous tears streaming down a banana yellow face feels downright disrespectful. Imagine posting a brow-furrowed Angry emoji in response to a friend’s personal story of sexual assault. It’s the symbolic equivalent of “that rascal!!” and woefully inadequate for anything that provokes real anger.

- Sheffield is on a quest to be the fairest city of them all – here’s how it’s doing — Rowland Atkinson and Alan Walker in the Conversation:

Led by the city council, several large employers have introduced a higher living wage based on calculations by the Living Wage Foundation, and the Sheffield Chamber of Commerce has also encouraged small and medium-sized organisations to do so. Another recommendation, on fair access to credit, resulted in the creation of Sheffield Money, to compete with the unscrupulous and usurious payday lenders. More recently, a fair employer charter was introduced, designed to ensure fair conditions of work as well as pay. Several large public and private organisations have already signed up to the charter, which focuses on promoting fair and flexible employment contracts.

- Eurozone’s So-Called Recovery Masks A Dark Secret: Mercantilism — John Weeks in Social Europe:

In the 18th century governments used direct restrictions on imports and other market interventions in an attempt to achieve permanent trade surpluses. Governments implement the 21st century version of mercantilism with different policy instruments. In the place of direct restrictions on trade we now see real wage reductions, manipulation of business taxes, and currency depreciation through loose monetary policy (so-called quantitative easing and negative interest rates). This “market friendly” version of mercantilism allows the ideologues to maintain the fiction of “free trade” while pursuing the mercantilist goal of persistent trade surpluses. This perverse inversion of rhetoric seeks to justify recovery in Europe based on beggar-thy-neighbour policies.

- Dean Rusk Also Missing, Feared Dead — for the Intercept, Barrett Brown reviews Niall Ferguson's fawning biography of Kissinger from his (Brown's) prison cell. Hilarity ensues:

[…] he noted that Kissinger had been described in disparaging terms by Hunter S. Thompson, who wrote about pretty much every major political figure in disparaging terms, and that he’d been denounced as a practicing Satanist by David Icke, who’s denounced pretty much every major political figure as a practicing Satanist; rather inexplicably, Ferguson himself even provided an incomplete list of over a dozen other prominent men and entire family dynasties against whom Icke has made this exact charge. It’s the first time I can recall having seen someone actually screw up anecdotal evidence […] Having returned from his cherry picking expedition with a basket full of rocks[…]

Sunday, 4 September 2016 - 6:52pm

This week, I have been mostly reading:

- Bank lending, quick macro recap — Warren Mosler:

Unsold output = rising inventories = cutbacks output = reduced income = reduced sales = reduced income = reduced sales = pro cyclical downward spiral, etc. as income reductions in one sector ‘spread’ to cuts into reduced sales in the rest. And it reverses only after deficit spending- public or private- gets large enough to offset desires to ‘save’/not spend income.

- Freedom and Intellectual Life — Zena Hitz in First Things (via Eric Schliesser):

It is removal of intellectual life from the world that accounts for its true inwardness—an inwardness distinct from the narcissistic inner tracking of one's social standing. It is the withdrawn person's independence from contests over wealth or status that provides or reveals a dignity that can't be ranked or traded. This dignity, along with the universality of the objects of the intellect—that is, that they are available to everyone—is what opens up space for real communion.

- We’re All Free Riders. Get over It! — Nicholas Gruen in Evonomics:

In addition to the free rider problem, which we should solve as best we can, there’s a free rider opportunity. And while we whine about the problem, the opportunity has always been far larger and its value grows with every passing day. […] We’re not paying royalties to the estates of Matthew Bolton and James Watt for their refinements to the piston engine. But we’re still free riding on their work. In other words, free-riding made us what we are today.

- Stop this cynical attack: Corbyn, anti-semitism and the right — the Jewish Socialists' Group, reposted in Counterfire:

The attack is coming from four main sources, who share agendas: to undermine Jeremy Corbyn as leader of Labour; to defend Israeli government policy from attack, however unjust, racist and harmful towards the Palestinian people; and to discredit those who make legitimate criticisms of Israeli policy or Zionism as a political ideology. As anti-racist and anti-fascist Jews who are also campaigning for peace with justice between Israelis and Palestinians, we entirely reject these cynical agendas that are being expressed by: • The Conservative Party • Conservative-supporting media in Britain and pro-Zionist Israeli media sources • Right-wing and pro-Zionist elements claiming to speak on behalf of the Jewish community • Opponents of Jeremy Corbyn within the Labour party.

- Ed Balls — Britney Summit-Gil muses on the significance of #EdBallsDay in Cyborgology:

Something that has struck me throughout this election season is the work that Bernie Sanders supporters have done digging up old video clips and transcripts to write narratives that are lacking in major news outlets. The fact that no millennial remembers a speech Sanders made before the Senate in 1992 does not preclude their ability to find it, watch it, and use it to make a political argument. This becomes all the more important when these narratives are lacking from other vehicles of mediated memory. In other words, if mainstream news sources are failing to remember important historical moments and contexts, the affordances of digital media offer an alternative.

- Leaked 2015 Memo Told Dems: 'Don't Offer Support' For Black Lives Matter Policy Positions — Julia Craven at the HuffPo:

“Presidential candidates have struggled to respond to tactics of the Black Lives Matter movement,” reads the memo, sent by a Democratic Congressional Campaign Committee staffer in November. “While there has been little engagement with House candidates, candidates and campaign staff should be prepared. This document should not be emailed or handed to anyone outside of the building. Please only give campaign staff these best practices in meetings or over the phone.”

- The national economic implications of a taco truck on every corner — Philip Bump at the Washington Post:

"My culture is a very dominant culture, and it's imposing — and it's causing problems," Marco Gutierrez of Latinos for Trump told Joy Ann Reid. "If you don't do something about it, you're going to have taco trucks on every corner." […] If you assume that three people work in each truck, that's 9.6 million new jobs created. The labor force in August was 159.4 million, with 144.6 million employed. Adding 9.6 million taco truck workers would help America reach nearly full employment — and that's just the staffing in the trucks. Think about all of the ancillary job creation: mechanics, gas station workers, Mexican food truck management executives. We'd likely need to increase immigration levels just to meet the demand.

[Personally, I'd prefer kebabs, though I suppose for Trumpists that would be even worse.] - Billionaire Nike Co-Founder Confuses His Net Worth with U.S. Economic Growth — Jon Schwarz, the Intercept :

For the GDP to triple in size in 22 years would require an average annual growth rate of over 5 percent — but the U.S. economy didn’t grow that fast, year over year, even once from 1994 to 2016. So how has Knight latched onto this blatantly wrong factoid? Possibly because there is something that’s tripled in size in the past 20 years: Knight’s own net worth. According to Forbes, Knight’s net worth in 1996 was, adjusted for inflation, about $8 billion; today it’s $25 billion. You can understand why he’d be convinced the economy is in great shape.

- The problems with Bitcoin — Richard Murphy delivers a devastating chartalist smackdown to the techno-utopian gold standard:

A blockchain where the extraction of value (the credit transactions) is not identified but where it is said that the supply of debits is finite (as the Bitcoin algorithm must imply) has at least three important economic characteristics that pose difficulties. One is that it attempts to mirror the operations of the gold standard, which proved to be little short of an economic disaster during its period of use in the twentieth century. Secondly, because of its opacity, the system is at best inherently risky. And third, it would appear that the arrangement could, because of its opacity, be exploited. I am not saying it is: I am saying that based on my initial review I have that concern.

- The American Jewish scholar behind Labour’s ‘antisemitism’ scandal breaks his silence — Jamie Stern-Weiner interviews Norm Finklestein on openDemocracy:

Compare the American scene. Our Corbyn is Bernie Sanders. In all the primaries in the US, Bernie has been sweeping the Arab and Muslim vote. It’s been a wondrous moment: the first Jewish presidential candidate in American history has forged a principled alliance with Arabs and Muslims. Meanwhile, what are the Blairite-Israel lobby creeps up to in the UK? They’re fanning the embers of hate and creating new discord between Jews and Muslims by going after Naz Shah, a Muslim woman who has attained public office. […] It’s time to put a stop to this periodic charade, because it ends up besmirching the victims of the Nazi holocaust, diverting from the real suffering of the Palestinian people, and poisoning relations between the Jewish and Muslim communities.

Sunday, 28 August 2016 - 8:11pm

This week, I have been mostly reading:

- Ramen is displacing tobacco as most popular US prison currency, study finds — Mazin Sidahmed, in the Guardian Holy cow; the one place where you can find a genuine commodity currency. But how do they buy noodles? With noodles?:

Ramen noodles are overtaking tobacco as the most popular currency in US prisons, according a new study released on Monday. A new report by Michael Gibson-Light, a doctoral candidate in the University of Arizona’s school of sociology, found the decline in quality and quantity of food available in prisons due to cost-cutting has made ramen noodles a valuable commodity.

- Caitlyn Jenner and Our Cognitive Dissonance — Robert Sapolsky in Nautilus:

Then there’s spotted hyenas, gender-bending pseudo-hermaphrodites. It’s nearly impossible to determine the sex of a hyena by just looking, as females are big and muscular (due to higher levels than males of some androgenic hormones), have fake scrotal sacs, and enlarged clitorises that can become as erect as the male’s penis. None of which was covered in The Lion King.

- Ideas for Australia: Welfare reform needs to be about improving well-being, not punishing the poor — Peter Whiteford in the Conversation:

The OECD report suggests the job-search requirements in Australia are more onerous than those in the other countries studied. In 2007, a jobseeker in Australia could be required to report between eight and 20 job-search activities each month, compared to four to ten each month in Switzerland, ten in the UK and only two in Japan. The OECD also notes that since 2000 there have been “vast swings” in sanction rates (penalties for non-compliance), with sanctions ranging in this period from 25,000 a year to 300,000.

- When Bitcoin Grows Up: What is Money? — John Lanchester in the London Review of Books:

Yap has no metal. There’s nothing to make into coins. What the Yapese do instead is sail 250 miles to an island called Palau, where there’s a particular kind of limestone not available on their home island. They quarry the limestone, and then shape it into circular wheel-like forms with a hole in the middle, called fei. Some of these fei stones are absolutely huge, fully 12 feet across. Then they sail the fei back to Yap, where they’re used as money. […] It has sometimes happened to the Yapese that their boats are hit by stormy weather on the way back from Palau, and to save their own lives, the men have to chuck the big stones overboard. But when they get back to Palau they report what happened, and everyone accepts it, and the ownership of the stone is assigned to whoever quarried it, and the stone can still be used as a valid form of money because ownership can be exchanged even though the actual stone is five miles down at the bottom of the Pacific.

- The era of predatory bureaucratization – An interview with David Graeber — Arthur De Grave in OuiShare:

Many expected Occupy to take a formal political form. True, it did not happen, but look at where we are 3.5 years later: in most countries where substantial popular movements happened, left parties are now switching to embrace these movements’ sensibilities (Greece, Spain, United States, etc.). Maybe it will take another 3.5 years for them to have an actual impact on policy making, but it seems to me like the natural path of things. […] Right now, the most important thing for anti-authoritarian and horizontal movements is to learn how to enter an alliance with those who are willing to work within the political system without compromising their own integrity.

- Fix our debt addiction to fix our economy — Michael Hudson:

As the “One Percent” of banks puts the “99 Percent” deeper into debt, financialization has become the major cause of increasing inequality of wealth and income. In due course, the amount of debt will exceed the economy’s ability to produce a large enough surplus to pay it back. This makes a financial breakdown inevitable.

- Krugman discovers the obvious — Alexander X. Douglas:

Here it is. There is no operational difference between: (a) the state spending, selling bonds to ‘fund’ its spending, and then buying back the bonds, and (b) the state spending and not issuing the bonds in the first place. This is a point economists outside the mainstream have been making for years […] It’s obvious when you think about it. Suppose I give you $100. Then I ‘borrow’ back the $100. Then I buy back the debt from you, for $100. Or suppose I just give you the $100.

- Branko Milanovic advocates reinventing apartheid — Chris Bertram at Crooked Timber:

Part of what’s going on here is the economist’s perspective on policy, which just focuses on net improvements in well-being or utility, with income serving as a proxy, and which doesn’t, therefore, see human beings as possessed of basic rights which it is impermissible to violate. Rather, all and any rights can be sacrificed on the altar of income improvement, just in case someone is poor and desperate enough to make a deal (who are we, paternalistically, to stop them?). The road to hell is paved with Pareto improvements.

- You May Hate Donald Trump. But Do You Want Facebook to Rig the Election Against Him? — Trevor Timm at the Guardian at Common Dreams:

As Gizmodo reported on Friday, “Last month, some Facebook employees used a company poll to ask [Facebook founder Mark] Zuckerberg whether the company should try ‘to help prevent President Trump in 2017’.” Facebook employees are probably just expressing the fear that millions of Americans have of the Republican demagogue. But while there’s no evidence that the company plans on taking anti-Trump action, the extraordinary ability that the social network has to manipulate millions of people with just a tweak to its algorithm is a serious cause for concern.

Sunday, 14 August 2016 - 4:36pm

This week, I have been mostly writing essays and cursing the Australian higher education system. I also thought this was delightful:

- Donald Trump is like a biased machine learning algorithm — Cathy "mathbabe" O'Neil:

What that translates to is a constant iterative process whereby he experiments with pushing the conversation this way or that, and he sees how the crowd responds. If they like it, he goes there. If they don’t respond, he never goes there again, because he doesn’t want to be boring. If they respond by getting agitated, that’s a lot better than being bored. That’s how he learns.

Sunday, 7 August 2016 - 8:05pm

This week, I have been mostly reading:

- Olivier Blanchard Is Worried About Inflation In Japan — Dean Baker, master of the political economy punchline, at CEPR (US):

Debt is just one way in which governments obligate their public to future payments. Patent and copyright monopolies commit the public to paying rents that greatly exceed the free market price for the protected products. In the United States these payments are approaching 2.0 percent of GDP ($360 billion a year) for prescription drugs alone. It is remarkable that public finance economists seem to almost completely ignore rents for patents and copyrights when considering the financial burdens of various governments.

- Young Iraqis Overwhelmingly Consider U.S. Their Enemy, Poll Says — Murtaza Hussain at the Intercept:

“For years, many have argued that Muslims and Arabs, like other humans, don’t appreciate being bombed or occupied,” says Haroon Moghul, a fellow at the Institute for Social Policy and Understanding. “Finally, we have a study to confirm this suspicion.” - What’s so Bad about the Gold Standard? — David Glasner:

The gold standard did play a major role in spreading the Depression. But the role was not just major; it was dominant. And the role of the gold standard in the Great Depression was not just to spread it; the role was, as Hawtrey and Cassel warned a decade before it happened, to cause it. The causal mechanism was that in restoring the gold standard, the various central banks linking their currencies to gold would increase their demands for gold reserves so substantially that the value of gold would rise back to its value before World War I, which was about double what it was after the war. […] The Great Depression was caused by a 50% increase in the value of gold that was the direct result of the restoration of the gold standard. […] the problem with gold is, first of all, that it does not guarantee that value of gold will be stable. The problem is exacerbated when central banks hold substantial gold reserves, which means that significant changes in the demand of central banks for gold reserves can have dramatic repercussions on the value of gold. Far from being a guarantee of price stability, the gold standard can be the source of price-level instability, depending on the policies adopted by individual central banks.

- Did Capitalism Fail? Looking Back Five Years After Lehman — Roman Frydman and Michael Goldberg at INET. As the title suggests, an oldie but a goody:

Market instability is thus integral to how capitalist economies allocate their savings. Given this, policymakers should intervene not because they have superior knowledge about asset values (in fact, no one does), but because profit-seeking market participants do not internalize the huge social costs associated with excessive upswings and downswings in prices. It is such excessive fluctuations, not deviations from some fanciful “true” value – whether of assets or of the unemployment rate – that Keynes believed policymakers should seek to mitigate. Unlike their successors, Keynes and Hayek understood that imperfect knowledge and non-routine change mean that policy rules, together with the variables underlying them, gain and lose relevance at times that no one can anticipate.

- The Market Fairy Will Not Solve the Problems of Uber and Lyft — Ian Welsh nails it:

These business models are ways of draining capital from the economy and putting them into the hands of a few investors and executives. They prey on desperate people who need money now, even if the money is insufficient to pay their total costs. Drivers are draining their own reserves to get cash now, but, hey, they gotta eat and pay the bills.

The model generalises to any low-paid insecure work. You can't afford to say no to even the worst job. I did it for nearly ten years, working harder than I'd ever worked in my life, and am now massively in debt, for the first time in my life. - The Zombie Doctrine — George Monbiot delivers some sublime ranting:

It’s as if the people of the Soviet Union had never heard of communism. The ideology that dominates our lives has, for most of us, no name. Mention it in conversation and you’ll be rewarded with a shrug. Even if your listeners have heard the term before, they will struggle to define it. Neoliberalism: do you know what it is?

- Who do faculty “work for?” — Historiann:

There’s nothing like stupid from the central administration to bring a faculty together. I told my colleagues that I have a rule when it comes to any technology or software: it works for me, I don’t work for it. End of story.

- A British Bridge for a Divided Europe — Robert Skidelsky:

The eurozone has weakened the nation-states comprising it, without creating a supranational state to replace the powers its members have lost. Legitimacy thus still resides at a level of political authority that has lost those attributes of sovereignty (such as the ability to alter exchange rates) from which legitimacy derives. […] The EU has tried to achieve political union incrementally, because it was impossible to start with it. Indeed, barely hidden in the “European project” was the expectation that successive crises would push political integration forward. This was certainly Jean Monnet’s hope. The alternative – that the crises would have the opposite effect, leading to the breakup of the economic and monetary union – was never seriously confronted.

- Patently Absurd Logic On Budget Deficits and Debt — Dean Baker at the Huffington Post:

As much as folks may love the private sector, it was not going to make up the demand lost when the housing bubble crashed, or at least not any time soon. If we wanted to prevent a long and severe downturn like the Great Depression, it was necessary for the government to run large deficits. These deficits were not impoverishing our kids - they were keeping their parents employed. […] The fact that the deficit hawks can scream endlessly about the horrible interest burden on our children, but don’t even seem to notice the costs being imposed by patent and copyright monopolies, suggests that they are not really concerned about our children’s well-being. Alternatively, they may have a very poor understanding of economics. Either way, their whining does not deserve the public’s attention.

- Where Hope Goes to Die — Ted Rall:

Sunday, 31 July 2016 - 5:49pm

This week, I have been mostly reading:

- Was the Financial Crisis Anticipated? — Ozlem Akin, José M Marín, and José-Luis Peydró at INET, on their CEPR (UK) working paper:

The paper finds that the top executives’ ex-ante sale of their own bank shares predicts worse bank returns during the crisis; interestingly, effects are insignificant for independent directors’ and other officers’ sales of shares. That is, effects are substantially stronger for the insiders with the highest and best level of information, the top five executives. Moreover, the top five executives’ impact is stronger for banks with higher ex-ante exposure to the real estate bubble, where an increase of one standard deviation of insider sales is associated with a 13.33 percentage point drop in stock returns during the crisis period. Our results suggest that insiders understood the heavy risk-taking in their banks; they were not simply over-optimistic, and hence they sold more of their own shares before the crisis.

- I’m With The Banned — Laurie Penny goes gonzo for Medium:

My new Spectator friend is as bewildered as I am by the way Americans take Milo and his ilk seriously, by their willingness to take pride in performative bigotry and call it strength. It works. It sells. It’s the unholy marriage of that soulless debate culture that works so well in Britain, transplanted to a nation with no social safety net and half a billion guns. It works, in part, because of the essentially cult-like nature of U.S. culture and the structured ignorance that accompanies it. America is a nation eaten by its own myth. The entire idea of America is about believing impossible things. Nobody said those things had to be benign.

- City Talk Pages — xkcd:

- Dana Milbank Tells Readers He Has an Incredibly Weak Imagination — Dean Baker, CEPR (US):

What is perhaps most incredible is Milbank's notion of irresponsible. His sole measure of responsibility is the size of the government budget deficit and debt, which are for all practical purposes meaningless numbers. (If the government puts in place patent protection that requires us to pay an extra $400 billion a year for prescription drugs, this adds zero to the budget deficit or debt and therefore doesn't concern Milbank. However, if it borrowed an extra $400 billion a year to pay for developing new drugs, he would be furious.)

- Now we’ve voted for Brexit, great British businesses like Southern rail, Byron burger, Lloyds bank and Sports Direct are finally set free — Mark Steel, whose voice you hear in your head as you're reading, in the Independent:

[T]he marvellous thing about privatisation is it introduces choice, so if customers trying to get from East Grinstead to London aren’t happy with their rail service, they can choose to use a different rail network, such as the one from Glasgow to Fort William, or the Trans-Siberian Express.

- Record Lows — Saturday Morning Breakfast Cereal:

- Embarrassment for Christine Lagarde and IMF as Fund's own watchdog slams its eurozone record — Ben Chu at the Independent:

The IEO concluded the IMF had “lost its characteristic agility as a crisis manager” in the way it responded to the economic turmoil in the eurozone, which required unprecedented bailouts for several states shut out of the capital markets and looked like it was going to tear the single currency zone apart.

[I don't know. They turned a disaster into an apocalypse in record time. If that's not "characteristic agility" I don't know what is.] - Our attitude towards wealth played a crucial role in Brexit. We need a rethink — Stephen hawking in the Guardian:

One of the reasons I believed it would be wrong to leave the EU was related to grants. British science needs all the money it can get, and one important source of such funding has for many years been the European commission. Without these grants, much important work would not and could not have happened. […] Money is also important because it is liberating for individuals. I have spoken in the past about my concern that government spending cuts in the UK will diminish support for disabled students, support that helped me during my career. In my case, of course, money has helped not only make my career possible but has also literally kept me alive.

- How to be a writer — The Oatmeal:

- “Liberal” Economists Cheered the New Democrats’ Deregulation of Finance — Bill Black at NEP:

Bill Clinton and Al Gore were two of the most powerful leaders of the “New Democrats” – a group of Democrats determined to move the party strongly to the right on economics, budget, national security, regulation, and crime. The New Democrats’ policy apparatus was funded overwhelmingly by Wall Street but its ideological support came from economists who were “liberal” on some social issues. The Clintons and Gore delivered for Wall Street by embracing the three “de’s” – deregulation, desupervision, and de facto decriminalization that encouraged and allowed twin bubble to rapidly expand. The “dot com” bubble was the first bubble to burst. The housing bubble burst in late 2006, leading to the financial crises of 2008 and the Great Recession that began in 2007.

Sunday, 24 July 2016 - 1:57pm

This week, I have been mostly… I don't know what I've been doing. Meanwhile, this happened in my sharply curtailed idle reading:

- Economic Rationality Explains Everything and Nothing — Geoffrey Hodgson, Evonomics:

Utility maximization can be useful as a heuristic modelling device. But strictly it does not explain any behavior. It does not identify specific causes. It cannot explain any particular behavior because it is consistent with any observable behavior. Its apparent universal power signals weakness, not strength.

- Everyone But the Media Saw Trumpism Coming — Ted Rall:

“We were largely oblivious to the pain among working-class Americans and thus didn’t appreciate how much his message resonated,” [New York Times journalist Nicholas] Kristof wrote. Most Americans are working-class. In other words, Kristof and his colleagues admit they don’t cover the problems that affect most Americans. Again: why does he still have a job?

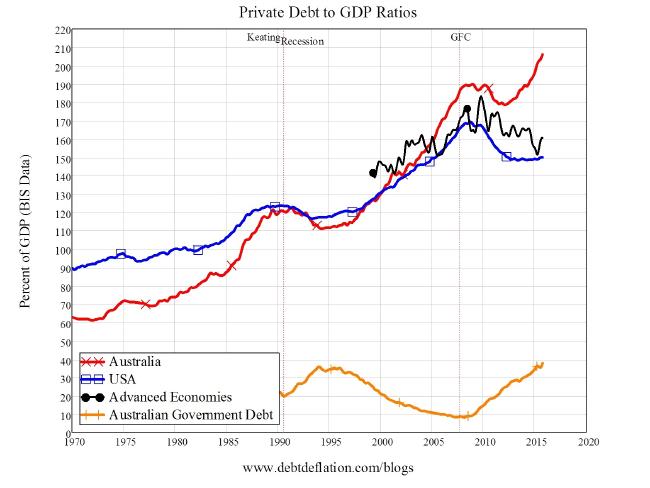

- Is an Aussie debt crisis around the corner? — Leith van Onselen, Macro Business:

Admittedly, the real concern is that 40% of all mortgages are interest-only mortgages, which are more vulnerable […] Whether or not Australia is likely to experience some kind of financial crisis within the next three years is a moot point. But having one of the world’s most overvalued housing markets, combined with overly indebted households and an extreme reliance on offshore funding, is hardly a good situation to be in and the opposite of prudence.

And… - The seven countries most vulnerable to a debt crisis — Steve Keen, Real World Economics Review Blog:

They are, in order of likely severity: China, Australia, Sweden, Hong Kong (though it might deserve first billing), Korea, Canada, and Norway. […] Timing precisely when these countries will have their recessions is not possible, because it depends on when the private sector’s willingness to borrow from the banks—and the banking sector’s willingness to lend—stops. This can be delayed by government policy—as it was in Australia in 2008, via a strong government stimulus, the restarting of the housing bubble by a government grant to first home buyers, and the boom in investment and exports set off by China’s own stimulus program. But the day when credit growth stops can’t be put off indefinitely. When it arrives, these countries—many of which appeared to avoid the worst of the crisis in 2008—will join the world’s long list of walking wounded economies.

- Are We Facing a Global “Lost Decade?" — Steve Keen, for the Private Debt Project [tl;dr: Yes.]:

The tragedy is that although there are methods by which we could escape the global private debt trap into which we have fallen we are nonetheless prisoners of an economic orthodoxy that will prevent us from employing them... The main barrier here is simply the ignorance of the supposed experts on economics about the nature of money. While mainstream economists continue to spout naïve arguments about money and banking, the politicians who rely upon them for guidance are unlikely to attempt anything other than the poorly targeted and largely ineffective policies that Japan has persisted with for the last quarter century. A global “Lost Decade” is entirely probable.

Sunday, 17 July 2016 - 5:18pm

This week, I have been mostly reading:

- Something Crazy Is Happening to Swiss Bonds, and It’s a Sad Sign for the World Economy — Jordan Weissmann at Slate:

Yields on government bonds from all around the world have been plunging thanks to anxious investors buying them for their safety. (Bond yields fall as prices rise.) And in many instances, the returns have cratered below zero. As Quartz reports Thursday, “around a third of all developed-country government debt—or more than $7 trillion, in terms of market value—is now trading at negative yields,” meaning that buyers are willing to pay more for these bonds than they will eventually get back if they hold them to maturity. […] The most mind-blowing example of this trend is Switzerland. Last week, yields on all of its government bonds, out to 50 years, turned negative.

[A major qualification: Government bonds aren't loans. Governments with their own currency never need to borrow money in order to spend. Bonds are a mechanism to drain reserves held at central banks, in order to hit interest rate targets. The pessimism is real, though.] - Corbyn: the summer of hierarchical things — Paul Mason in Medium:

By September, if Corbyn wins he’ll be in a position to go into the Labour conference exerting control: over the NEC, where a left slate looks likely to win; and over policy via conference, where the delegates will for the first time reflect the changed membership. After that, in any election called by the incoming Tory prime minister Theresa May, Corbyn’s supporters would be able to stage “trigger ballots” to de-select the MPs most hostile to Corbyn, leaving the leadership, the HQ, the policy and the parliamentary group aligned to the left.

- Donald Trump Understands the Nexus Between Trade and Immigration — a corker by Marshall Auerback in Naked Capitalism:

Historically, immigration law has concerned itself with many considerations, the most of which is the displacement of US workers. By contrast, advocates of free trade ignore this consideration, or blithely suggest that the resultant unemployment in a displaced sector (e.g., the automobile industry), is a “negative externality”, which is generally offset by the resultant gains in competitive efficiency, and lower cost goods. Cheap imports, then, outweigh the displacement of workers. But we do not extend this logic to immigration, or we would move straight to a policy of open borders.

- The murky world of industrial relations in the higher ed sector — Joanne Finkelstein in On Line Opinion:

The quality of universities' delivery to students is adversely influenced by the casual, less engaged and experienced academic. It is particularly evident in newer institutions which have been aggressive in developing new programs of study supposedly in response to market demands. […] in the higher education sector, such a culture has ensured a declining quality in teaching especially in the newer and regional universities – those institutions designed specifically to widen participation and increase social equity.

- Modern Money: The Basics — Geoff Coventry provides a really nice, concise summary I wish I'd written:

Money is a wonderful human invention – perhaps one of our greatest. Most nations have a monetary system designed to provide for private commercial needs, but also, simultaneously, to enable governments to access sufficient resources to create safe, just and ever-improving societies.

- Bernie Sanders’ connections with two UMKC economists run deep — Mark Davis at the Kansas City Star does a charming local news profile of Stephanie Kelton and Bill Black:

Kelton and Black are part of a team of economic advisers, including former labor secretary Robert Reich and James Galbraith at the University of Texas in Austin, who help the Sanders campaign develop policies. Randall Wray, a fellow UMKC economics professor, credits Sanders for embracing thinkers from outside the economic mainstream. “The mainstream is a complete disaster and a complete disaster for our country,” Wray said.

[We can assume they won't be advising Clinton.] - Note To Economists: Saving Doesn’t Create Savings — Steve Roth in Evonomics;another wonderfully concise explanation I wish I'd written:

When you spend money — transferring it to someone else in return for newly-produced goods and services — does it affect our collective monetary savings? In strict accounting terms, obviously not. Your money just moves from your account to someone else’s account; it doesn’t disappear. Your bank has less deposits; the recipient’s bank has more deposits. Aggregate monetary savings is unchanged by that accounting event. […] In three simple words: spending causes saving. Real, collective accumulation of real, long-lived stuff. Monetary saving — not-spending part of your income this year — doesn’t, collectively, create either real or monetary savings.

- How Democrats Created Liberalism of the Rich — Thomas Frank, Naked Capitalism via TomDispatch:

Boston is the headquarters for two industries that are steadily bankrupting middle America: big learning and big medicine, both of them imposing costs that everyone else is basically required to pay and which increase at a far more rapid pace than wages or inflation. A thousand dollars a pill, 30 grand a semester: the debts that are gradually choking the life out of people where you live are what has made this city so very rich. […] Professional-class liberals aren’t really alarmed by oversized rewards for society’s winners. On the contrary, this seems natural to them — because they are society’s winners. The liberalism of professionals just does not extend to matters of inequality; this is the area where soft hearts abruptly turn hard.

- Letter from US Senator Al Franken to Niantic, Inc., owners of Pokemon GO:

Recent reports, as well as Pokemon GO s own privacy policy, suggest that Niantic can collect a broad swath of personal information from its players. From a user's general profile information to their precise location data and device identifiers, Niantic has access to a significant amount of information, unless users - many of whom are children - opt-out of this collection. Pokemon GO'S privacy policy states that all of this information can then be shared with The Pokemon Company and "third party service providers", details for which are not provided, and farther indicates that Pokemon GO may share de-identified or aggregated data with other third parties for a non-exhaustive list of purposes. Finally, Pokemon GO s privacy policy specifically states that any information collected - including a child's - "is considered to be a business asset" and will thus be disclosed or transferred to a third party in the event that Niantic is party to a merger, acquisition, or other business transaction.

- Privatisation! Free trade! Shares for all! The great con that ruined Britain — Peter Hitchens in the Daily Mail! (via Richard Murphy):

I am so sorry now that I fell for the great Thatcher-Reagan promise. […] I thought – this now seems especially funny – that private British Telecom would be automatically better than crabby old Post Office Telephones. I think anyone who has ever tried to contact BT when things go wrong would now happily go back to the days of nationalisation. Soviet-style slowness was bad, but surely better than total indifference.

- Is Competition the Cause of the Productivity Slowdown? — Dean Baker, CEPR:

My alternative explanation is that a weak labor market and low wages explain much of the slowdown in productivity. The argument is straightforward. When Walmart can hire people at very low wages, they are happy to pay people to stand around and do almost nothing. That is why many retailers now have greeters or sales people standing in aisles who contribute little to productivity.

Sunday, 10 July 2016 - 4:07pm

This week, I have been mostly reading:

- Psychologists Throw Open The “File Drawer” — Neuroskeptic:

Now, a group of Belgian psychology researchers have decided to make a stand. In a bold move against publication bias, they’ve thrown open their own file drawer. In the new paper, Anthony Lane and colleagues from the Université catholique de Louvain say that they’ve realized that over the years, “our publication portfolio has become less and less representative of our actual findings”. Therefore, they “decided to get these [unpublished] studies out of our drawer and encourage other laboratories to do the same.”

- Insanity — xkcd:

- Reform School — Malcolm Harris at The New Inquiry reviews Schools on Trial, by Nikhil Goyal:

In 1837, Horace Mann, the founder of American compulsory education, established the Massachusetts Board of Education, the first such agency and one which would become the model for the nation. But Mann didn’t want a more intellectually engaged population—literacy in the state already stood at 99 percent. Social control was a serious concern for Western elites after a series of failed revolutions, and Mann was very impressed by the system he saw on a visit to Prussia. He returned with a plan for public education. “Compulsory schooling evangelists,” Goyal writes, “which included many industrialists and financiers, in fact, wanted to ‘dumb down’ the American population to create docile followers, not potentially troublesome freethinkers who questioned authority.”

- Trade Treaty Propaganda Goes Into High Gear — Dean Baker, CEPR:

As far as the protectionism in the TPP, the deal is quite explicitly about increasing the length and strength of patent and copyright protection. Yes, that is "protection" as in "protectionism." Patent and copyright protection do serve a purpose in providing an incentive for innovation and creative work, but all forms of protection serve a purpose. The question that serious people ask is whether there is a better way to serve the purpose.

- 'I Love My Label': Resisting the Pre-Packaged Sound in Ed-Tech — Audrey Watters:

As someone who works outside of academia, without an institutional affiliation, I can’t begin to tell you how frustrating it is to be unable to access journal articles. I always get so irked when I hear technology evangelists proclaim “You can learn anything you want on the Internet.” No, you can’t. Huge swaths of knowledge, art, science remain inaccessible; and it’s a loss for scholarship, which need not and does not only happen among those with access to a university research library or with log-in credentials to its online portal. That inaccessibility is a reflection of institutional culture, industry culture, corporate culture, copyright (that is, intellectual property laws), capitalism, and code. That is, when we talk about the future of something like “education technology” or even when we talk about the future of research and scholarship or teaching and learning, we must grapple with issues that are technological, sociological, and above all, ideological.

- The elites hate Momentum and the Corbynites - and I’ll tell you why — David Graeber, providing "opinion" for The Guardian, as opposed to whatever the hell you'd call the utter tripe they normally publish about Corbyn:

I’ve spent much of the past two decades working in movements aimed at creating new forms of bottom-up democracy, from the Global Justice Movement to Occupy Wall Street. It was our strong conviction that real, direct democracy, could never be created inside the structures of government. One had to open up a space outside. The Corbynistas are trying to prove us wrong. Will they be successful? I have absolutely no idea. But I cannot help find it a fascinating historical experiment. […] insofar as politics is a game of personalities, of scandals, foibles and acts of “leadership”, political journalists are not just the referees – in a real sense they are the field on which the game is played. Democratisation would turn them into reporters once again, in much the same way as it would turn politicians into representatives. In either case, it would mark a dramatic decline in personal power and influence. It would mark an equally dramatic rise in power for unions, constituent councils, and local activists – the very people who have rallied to Corbyn’s support.

- The Duncan Smith resignation: fundamentally shifting the economic debate — Neil Schofield:

'I am unable to watch passively whilst certain policies are enacted in order to meet the fiscal self imposed restraints that I believe are more and more perceived as distinctly political rather than in the national economic interest.' In other words, for the first time a key player in the post-2010 Conservative project has said, almost explicitly, that austerity is a political, not an economic choice. […] In other words, Duncan Smith’s resignation letter – and the events surrounding it – powerfully endorse the fundamental tenet of Jeremy Corbyn’s and John McDonnell’s economic programme: that austerity is a choice, not an economic necessity. It wholly destroys the intellectual underpinning of McDonnell’s opponents in the Parliamentary Labour Party.

- Peak Indifference — Cory Doctorow in Locus Online:

At a certain point, indifference to tobacco’s dangers peaked – long before actual tobacco use peaked. Peak indifference marks a turning point. […] That’s why it’s time for privacy activists to start thinking of new tactics. We are past peak indifference to online surveillance: that means that there will never be a moment after today in which fewer people are alarmed by the costs of surveillance.

- A world war has begun. Break the silence. — John Pilger:

In 2009, President Obama stood before an adoring crowd in the centre of Prague, in the heart of Europe. He pledged himself to make "the world free from nuclear weapons". People cheered and some cried. A torrent of platitudes flowed from the media. Obama was subsequently awarded the Nobel Peace Prize. It was all fake. He was lying. The Obama administration has built more nuclear weapons, more nuclear warheads, more nuclear delivery systems, more nuclear factories. Nuclear warhead spending alone rose higher under Obama than under any American president.

- Budget accounting tricks — Simon Wren-Lewis:

One of the problems with fixed date deficit (or in this case surplus) targets is that they encourage playing around with the public finances to hit the target. Generally, but not always, this involves making a saving today by shifting costs into the future. Privatisation is an obvious example. It may be justified if the net present value of the sale is positive, or if privatisation really improves efficiency, but all to [sic] often it is a device to meet a short term target.

Although a New Keynesian (Wren-Lewis will when pressed admit he subscribes to the superstition of "sound finance"), he makes a good point here. i.e. that, just as in the popular bugaboo where public deficits can be run up by unscrupulous pollies who "buy votes", those same unscrupulous pollies are more likely in the current neoliberal environment to buy a reputation as good economic managers by using fire sales of public assets (usually a bad thing) to hide deficits (rarely a bad thing). - Get ready for a recession by 2017 — Steve Keen in the Australian:

Whichever party is in opposition at the time will blame the incumbent, but in reality this recession has been set up by the sidestep both parties have used to avoid downturns for the past quarter century: whenever a crisis has loomed, they’ve avoided recession by encouraging the private sector to borrow and spend. […] Australia’s most famous recession sidestep was during the GFC, when it was one of only two countries in the OECD to avoid experiencing two consecutive quarters of negative GDP growth (the other country was South Korea). Since then, the private sectors of the advanced countries have collectively de-levered, reducing their debt levels from about 170 to 160 per cent of GDP. Australia, in stark contrast, has levered up.

- Tony Blair's spin unspun: how his claims compare with the Chilcot report — Andy McSmith, The Independent:

Mr Blair has claimed that he was promising the Americans his support as a way of influencing Washington’s decision making and getting them to seek United Nations approval before acting. Taking questions from journalists, he asserted that his support was not “unconditional”. But the opening words of that July note [to Bush] – “I will be with you, whatever” – do sound unconditional.

- I read the Chilcot report as I travelled across Syria this week and saw for myself what Blair's actions caused — Robert Fisk, The Independent:

When Blair can say, as he did the moment the Chilcot report was published, that it should “lay to rest allegations [sic] of bad faith, lies and deceit” – without a revolution in the streets against his bad faith, lies and deceit – then you can be sure that his successors will have no hesitation in swindling the public again and again. After all, what’s the difference between Iraqi WMDs that don’t exist, 45-minute warnings that are falsities, 70,000 non-existent Syrian “moderates” and a fictitious NHS windfall of millions if Britain left the European Union?

- To Save The Economy, We Have To Break Its One Sacred Rule — Jason Hickel, Co.Exist:

As soon as we start focusing on GDP growth, we’re not only promoting the things that GDP measures, we’re promoting the indefinite increase of those things. And that’s exactly what we started to do in the 1960s. GDP was adopted during the Cold War for the sake of adjudicating the grand pissing match between the West and the USSR. Suddenly, politicians on both sides became feverish about promoting GDP growth. GDP growth became a sacred rule. And we remain in thrall to it today.

- Mocked and forgotten: who will speak for the American white working class? — Chris Arnade in The Guardian:

America, and particularly the white working class, is dealing with a drug epidemic that is killing more people each year at a startling rate. Just in the past decade deaths from drugs has doubled. The National Review sees it as another sign of the flawed character of the poor. This is a common and moralistic trope those battling an addiction have long dealt with – that it is all the fault of their weakness. The reality is often far more complex. Addiction thrives in societies undergoing stress.

- Stopping Deflation? Dead Easy. So Why Isn’t It Being Done? — Ian Welsh:

If you let fixed costs have inflation above income increases, then everything else is going to have to suffer deflation, because it is discretionary. Gotta eat and have a warm place to sleep, first.

- The Tory leadership election is a sort of X Factor for choosing the antichrist — Frankie Boyle in the otherwise disgraceful, paper of choice for the discerning New Labour war criminal, The Guardian:

[The Parliamentary Labour Party] say they need a leader who knows how to oppose, albeit primarily their own party membership. The idea is that Corbyn is unelectable, and it’s just one of life’s sad ironies that none of the people who believe this will be able to beat him in an election. […] One of the PLP’s main worries will be that Labour’s vote will crumble to Ukip under Corbyn, who won’t produce enough racist mugs and mouse mats to reassure everybody. And, to be fair, it must be galling to a party that invaded Iraq, rendered Libyans to be tortured by Gaddafi and detained asylum seekers with Dickensian cruelty to lose voters on the race issue.